by Sonam Srivastava, Siddharth Singh Bhaisora

Published On Sept. 10, 2023

Looking at people’s portfolios is routine for us. Last week, I looked over at my friend’s portfolio and it had over 100 stocks in it. Is 100 stocks too many? Is there such a thing as an over-diversified portfolio? Does concentration work better than diversification? Let’s look at it.

In our world, diversification is known as the “only free lunch” - if you don't know anything about investing, you will start with understanding diversification - add more stocks to diversify your portfolio as a failsafe way to mitigate risk. Of course, it is a bit more complicated than that, but for a layman that’s the gist of it. Now when we are constructing a portfolio, we try to optimize risk against the reward. As we add more stocks into a portfolio, the magic of diversification helps reduce the risk of holding any 1 stock i.e. stock specific risks decrease.

Here are a few scenarios -

High Prospective Returns Across the Board: When there are ample opportunities in the market with promising returns, diversification is beneficial. Since adding a new stock into a portfolio can improve returns without increasing the risk. In such markets, spreading investments is not just safe, but advisable

Diminishing Returns with Each New Investment: When each new investment promises a lower return for a given risk than the last, diversification can be detrimental. In such scenarios a concentrated portfolio could provide better returns.

Excess Diversification Hurts Returns, Rather than Reducing Risk: When the number of stocks are so many, that it becomes difficult to track or conduct deep research as an individual - there is a problem. This problem gets worse, if each stock added is of lower value than what is already present in the portfolio. In such scenarios, reducing to an optimal level is probably the right approach.

If you have a robo-advisory service like Wright Research , then this analysis is much easier since we run several algorithms, quantitative research, deep ML & AI Models to do our analysis - Technology does help solve part of the problem for point 3 above.

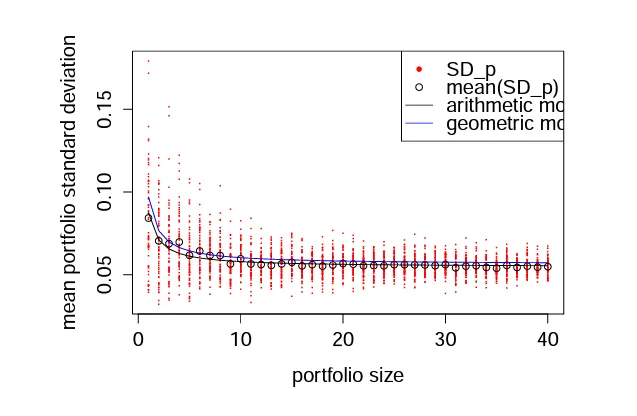

What is evident from this is that there is this concept of diminishing returns to adding another stock to a portfolio as diversification benefits taper off as we add more stocks to a portfolio. Here’s a graph that illustrates this concept better - we look at the mean portfolio standard deviation (risk) against the portfolio size (number of stocks held in that portfolio)

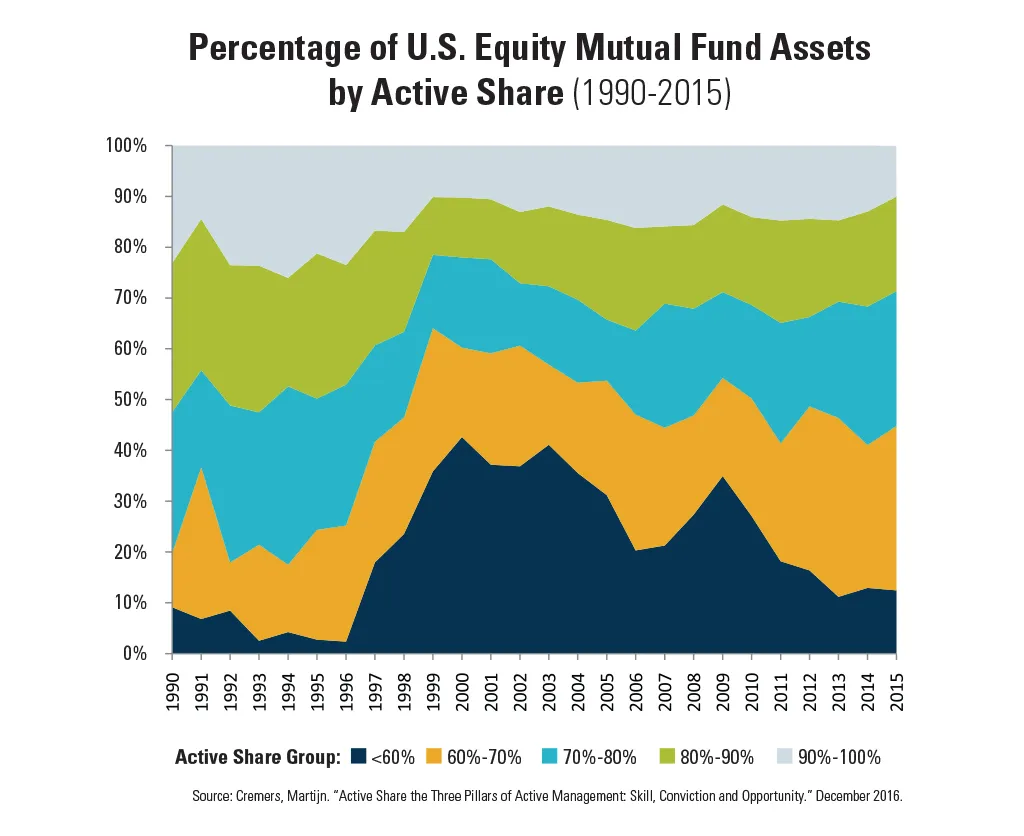

A Yale study from 2006 coined the term "active share" - how much the fund’s holdings differ from its benchmark index. The study found mutual funds with low active share (less than 60%) significantly underperformed their benchmarks by 1.37% per year. This underperformance was especially pronounced among small-cap managers but was also observed in large-cap funds. Problem with low active share funds is that fees are comparable to actively managed funds, but performance rarely deviates from their benchmark - so you are essentially paying for underperformance.

Other studies have supported the notion that concentrated portfolios—those where the fund manager places significant bets on a small number of stocks—are more likely to outperform. One study identified the "best ideas" within fund managers' portfolios by assessing position weights relative to their benchmarks. These "best ideas" outperformed other positions in the portfolio by 1.6% to 2.6% per quarter. Another research piece found that fund managers with concentrated portfolios outperformed their diversified counterparts by about 4% annually, attributing this superior performance specifically to their largest holdings.

Despite the evidence supporting concentrated portfolios, large fund managers often opt for overdiversification.

Maximize fee revenue: a more diversified portfolio allows for a larger fund size, thereby increasing fee income.

Risk aversion: managers who underperform their benchmarks dramatically risk losing their jobs, so maintaining a diversified portfolio can serve as a safety net.

Institutional constraints: Large funds, such as Mutual Funds, are often limited to investing in the most widely owned and analyzed stocks, which naturally leads to a more diversified portfolio.

Funds may also choose diversification to appear attractive on specific metrics like the Sharpe ratio, despite evidence that this can dilute performance.

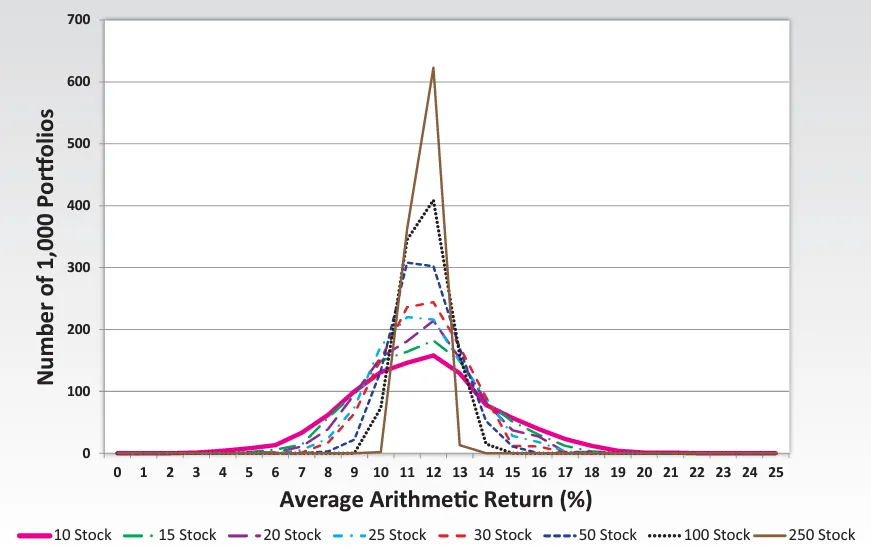

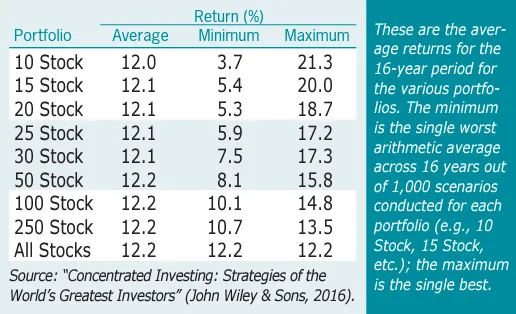

It depends. Fund managers may call a 25-35 stock portfolio as 'concentrated,' and anything over 45-50 as being over-diversified and some others may think 10-20 stocks is concentrated, and anything over 35 is excess diversification. In both scenarios 100 does sounds like too many. Here’s the findings from a research paper from John Wiley & Sons, 2016 -

The study analyzed average returns of portfolios containing between 10 and 250 stocks, randomly selected from the S&P 500 index.

They created 1,000 portfolios for each of the 8 different sized portfolios starting from 10 stocks to 15 stocks, 20, 25, 30, 50, 100 upto 250 stocks.

Unsurprisingly, portfolios comprising 250 stocks closely matched the performance of the S&P 500 equal-weight index, suggesting lower volatility.

In contrast, the pink line is shorter and wider for the 10-stock portfolios meaning it had a much broader range of returns, indicating a higher potential for divergence from the index performance.

The 10-stock portfolio generated a lowest return of 3.7% and the highest return of 21.3% while the 250 stock portfolio generated the lowest return of 10.7% and the highest return of 13.5%.

The ideology behind concentrated investing really stemmed from Sir John Maynard Keynes, an economist and the author of “The General Theory of Employment, Interest and Money”,1936, and Benjamin Graham, author of the pivotal book “Security Analysis”, 1934. This extract from Keynes, in a 1934 letter, shows his thoughts about a concentrated portfolio -

“As time goes on, I get more and more convinced that the right method in investment is to put fairly large sums into enterprises which one thinks one knows something about and in the management of which one thoroughly believes. It is a mistake to think that one limits one’s risk by spreading too much between enterprises about which one knows little and has no reason for special confidence… there are seldom more than two or three enterprises at any given time in which I personally feel myself entitled to put full confidence.”

Over time, other investors such as Warren Buffett, Charlie Munger and others have followed and stuck by the concentrated portfolio approach. As of May 2023, 63% of Berkshire Hathaway’s investment portfolio of $333.4 Billion was comprised of just 3 stocks. The mantra for proponents of concentrated investors is - Hold fewer but stronger stocks for longer periods to both mitigate risk and amplify returns. The Catch - Risk of 1 or 2 poor performing stocks impacting the portfolio’s performance. There is an argument that good picks may compensate for underperformance over sufficient time - but what is sufficient time?

A concentrated portfolio focuses on a limited number of high-conviction investments, typically comprising a small selection of stocks or assets. This investment approach allows investors to thoroughly research and understand each holding, thereby aiming to achieve superior returns by capitalizing on their deep knowledge and insights. Unlike diversified portfolios, which spread risk across numerous investments, a concentrated portfolio accepts higher risk in exchange for potentially higher rewards. This strategy can be particularly effective for skilled investors with strong confidence in their market analysis and the chosen assets' growth potential. However, it also requires careful monitoring and a robust risk management plan to mitigate potential downsides from lack of diversification.

Fund managers have different strategies for picking stocks. Depending on how strongly a manager feels about certain stocks over others, the number of stocks in a portfolio can vary.

If a manager strongly favors some stocks over others, it's better to have a smaller portfolio. Initially, adding more stocks reduces risk without sacrificing much in terms of potential returns. However, after a certain point, adding more stocks can actually lower the expected returns without significantly reducing risk. In such a case a concentrated portfolio of say 10 stocks is about as concentrated as we can get while maintaining some diversification benefits that help remove sufficient stock specific risk, and thus reduce the overall portfolio risk.

On the other hand, if a manager feels almost equally good about a larger set of stocks, then a bigger portfolio can be advantageous. Adding more stocks continues to reduce risk without hurting potential returns. In such a scenario, a portfolio of around 20 to 25 stocks could be optimal.

In both cases, the aim is to balance risk and reward effectively. The number of stocks in the portfolio will depend on how selective the manager is about the stocks they are choosing.

Holding fewer stocks does come with its own headache and anxiety - we have seen how varied the returns can be in the study above. And adding too many stocks can drag the portfolio’s performance. Concentrated portfolios are a useful approach for savvy investors who can conduct their own research and are able to discern between potential winners and losers - and thus can take calculated risks.

For retail investors, who aren’t as savvy or lack the time or expertise to research thoroughly - concentration could very well be an unacceptable level of risk if they are doing it on their own. Starting with mutual funds - consider concentrating them to a select few as opposed to having 6 or more mutual funds. Most mutual funds already provide sufficient diversification and having a few will cushion the portfolio - provided there is minimal overlap between the constituents or sectors the fund has invested in. Now, for investing in equities - consider a few equity baskets or smallcases that cater to your specific goals - but also look at a few concentrated portfolios if you have the risk appetite - they very well could help boost the portfolio.

Diversification is seen as a free lunch - but there are no free lunches, not in investing.

Diminished Returns: Over-diversifying can lead to average or below-average performance.

Complexity: Managing many assets increases the risk of errors and oversight.

Costs: More stocks often mean more transaction fees, reducing net returns.

Lack of Focus: Diversification can dilute the impact of top-performing stocks.

Overconfidence: A diversified portfolio may lead to a false sense of security, reducing vigilance.

Remember, diversification is a tool, not a guarantee. Always consider these risks when diversifying your portfolio.

At Wright Research, our philosophy is that markets are inherently dynamic - changes and abrupt shifts can be triggered by fast-changing macroeconomic factors, geopolitical climate, regulatory policies etc. and require us to be nimble and adapt our investment strategy accordingly. How do we do this? We use predictive machine learning models and AI technology, combining fast-moving macroeconomic variables and technical indicators over the index, to predict future market events. This highly accurate predictive model enables us to adapt our participation in various strategies dynamically. As market dynamics evolve, it's vital to adjust our strategies proactively. Alpha Prime is our high risk, high reward concentrated portfolio that responds to these changing dynamics.

An aggressive high risk, high reward momentum investing strategy, that focuses on only 10 top performing and trending stocks that have been specially chosen. Each stock added to the Alpha Prime portfolio demonstrates strong earnings momentum, fundamentals and key trending opportunities. The goal of Alpha Prime is threefold:

Build a robust concentrated portfolio designed for bull markets, capable of embracing concentrated risks for maximal returns.

Offer a concentrated portfolio specifically tailored for high-risk takers, seeking to exploit market trends to their full advantage.

To combine robust risk management with alpha and high trend investing to protect capital.

The concentrated momentum strategy of Alpha Prime aims for exceptional returns by focusing on a few top performing, high momentum stocks. While this approach offers the chance for higher gains, it also comes with higher risk. However, if selected stocks do well, then this concentrated portfolio’s benefits could significantly outweigh the associated risks.

The potential to generate alpha in our Alpha Prime strategy comes from a blend of expert portfolio design, experienced investment management, sophisticated quantitative models, and the use of AI technology for advanced market forecasting. We consciously forego certain diversification benefits to unlock higher potential returns for our investors. The following components form the core of our investment universe:

High momentum stocks for higher returns

Rigorous selection process identifying 10 stocks from top 500 companies

Use of AI Technology to identify market trends, anticipate market shifts, and adjust our portfolio strategy.

Risk optimization to balance reward-to-risk ratio

Diversification in a concentrated portfolio by not overly relying on any single stock or sector

Systematic deallocation in high-risk market scenarios

Return performance (in % terms) of the Alpha Prime Portfolio against its benchmark, Multicap Index is -

Over a 3 year horizon, ₹1 Lac invested would have become -

Here are the key performance metrics of the Alpha Prime Portfolio against its benchmark, the Multicap Index -

Explore the Alpha Prime Smallcase and the Wright Alpha Prime PMS Fund.

Watch the full video on the Dilemma of Portfolio Diversification: Understanding Concentrated Portfolios - Alpha Prime

Want to learn more about Alpha Prime, check out these articles -

Written by Sonam Srivastava, Siddharth Singh Bhaisora

Discover investment portfolios that are designed for maximum returns at low risk.

Learn how we choose the right asset mix for your risk profile across all market conditions.

Get weekly market insights and facts right in your inbox

It depicts the actual and verifiable returns generated by the portfolios of SEBI registered entities. Live performance does not include any backtested data or claim and does not guarantee future returns.

By proceeding, you understand that investments are subjected to market risks and agree that returns shown on the platform were not used as an advertisement or promotion to influence your investment decisions.

"I was drawn to Wright Research due to its multi-factor approach. Their Balanced MFT is an excellent product."

By Prashant Sharma

CTO, Zydus

By signing up, you agree to our Terms and Privacy Policy

"I was drawn to Wright Research due to its multi-factor approach. Their Balanced MFT is an excellent product."

By Prashant Sharma

CTO, Zydus

Skip Password

By signing up, you agree to our Terms and Privacy Policy

"I was drawn to Wright Research due to its multi-factor approach. Their Balanced MFT is an excellent product."

By Prashant Sharma

CTO, Zydus

"I was drawn to Wright Research due to its multi-factor approach. Their Balanced MFT is an excellent product."

By Prashant Sharma

CTO, Zydus

Log in with Password →

By logging in, you agree to our Terms and Privacy Policy

"I was drawn to Wright Research due to its multi-factor approach. Their Balanced MFT is an excellent product."

By Prashant Sharma

CTO, Zydus

Log in with OTP →

By logging in, you agree to our Terms and Privacy Policy

"I was drawn to Wright Research due to its multi-factor approach. Their Balanced MFT is an excellent product."

By Prashant Sharma

CTO, Zydus

Answer these questions to get a personalized portfolio or skip to see trending portfolios.

Answer these questions to get a personalized portfolio or skip to see trending portfolios.

(You can choose multiple options)

Answer these questions to get a personalized portfolio or skip to see trending portfolios.

Answer these questions to get a personalized portfolio or skip to see trending portfolios.

Answer these questions to get a personalized portfolio or skip to see trending portfolios.

(You can choose multiple options)

Investor Profile Score

We've tailored Portfolio Management services for your profile.

View Recommended Portfolios Restart