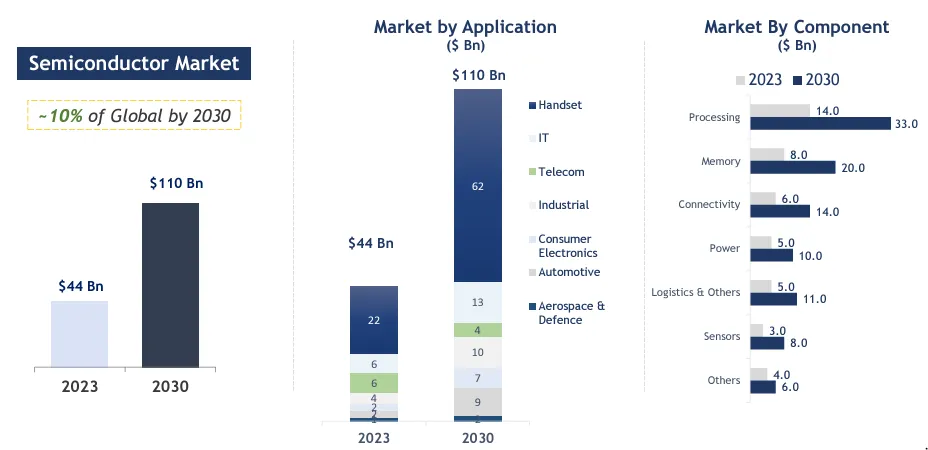

India is rapidly emerging as a global hub for semiconductor manufacturing, driven by significant government initiatives and growing international collaborations. According to a joint report by the India Electronics and Semiconductor Association, the country’s semiconductor consumption is set to increase from $22 billion in 2019 to $64 billion by 2026 - a 16% CAGR. By 2030, semiconductor consumption is projected to nearly double again to $110 billion, positioning India to account for approximately 10% of global semiconductor demand.

India currently contributes 20% of the global semiconductor design talent, with over 35,000 engineers engaged in chip design. With strategic partnerships with global technology leaders such as PSMC (Taiwan) and Synopsys (USA), and collaborations with countries like the US and Japan, India is poised to establish itself as a critical player in the global semiconductor value chain. Let’s look at the semiconductor industry in detail today.

Demand For Semiconductors Driven By Key Market Segments

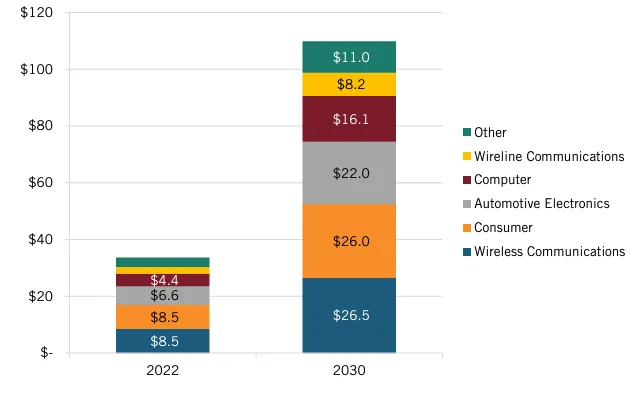

Official statistics show that only around 4 percent of global semiconductor sales occurred in India in 2022. However, the country actually accounts for about 10 percent of real global consumption. This discrepancy arises because many semiconductors sold in regions like Hong Kong or Singapore are ultimately integrated into products manufactured in India. Although these products may be exported, the initial semiconductor transformation or installation happens domestically, highlighting India's significant role in the global supply chain. By 2030, the largest segments of India's semiconductor market are expected to be:

Wireless Communications: $26.5 billion

Consumer Goods: $26 billion

Automotives: $22 billion

As of 2021, only 9% of semiconductor components used in India were locally sourced. However, there are plans to increase this to 17% by 2026. This would result in a 6x increase in locally sourced semiconductor revenue compared to 2019 levels. Despite these efforts, India still largely depends on imports for its semiconductor needs.

Electronics Production Booms

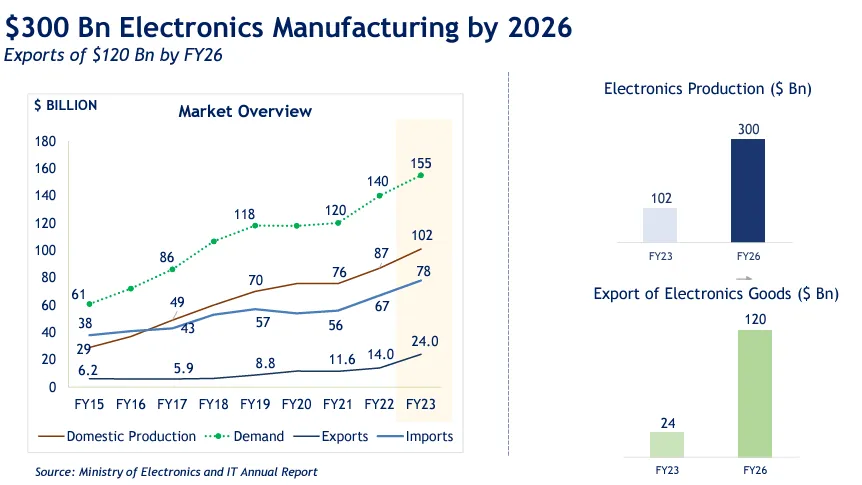

India’s electronics production , valued at $101 billion in 2022, is projected to triple to $300 billion by 2026 and to 5x to $500 billion by 2030. This will create over 6 million jobs in the process. A major contributor to this growth is the mobile phone sector, where production is expected to increase from $44 billion in 2023 to $110 billion by 2026. India has already become the world’s second-largest mobile phone manufacturer, doubling its share of global smartphone production to 19% over the past five years.

India’s electronics exports have shown remarkable growth, tripling from March 2018 to April 2023. Further expansion is expected, with exports projected to increase nearly fivefold from $25 billion in FY 2023 to $120 billion in FY 2026. This surge in exports aligns with India's overall merchandise export performance, which has consistently exceeded $100 billion quarterly since Q2 FY 2022.

Global Semiconductor Value Chain

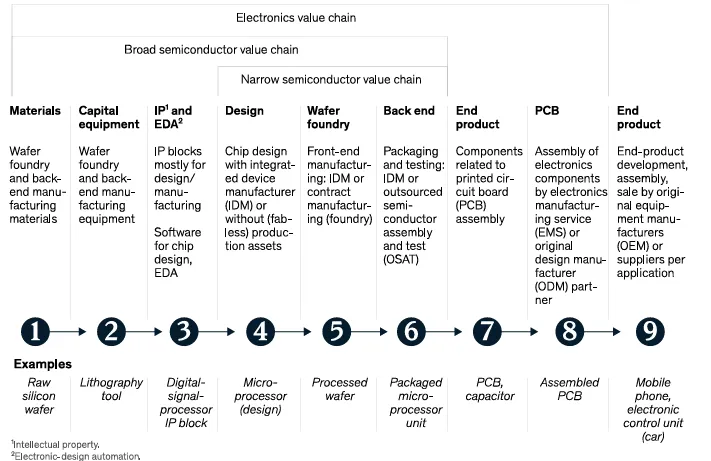

The semiconductor value chain is highly complex, involving a multitude of distinct stages that are geographically dispersed. The chain spans from material procurement to end-product manufacturing, with key processes including semiconductor R&D and chip design, fabrication, and assembly, testing, and packaging (ATP).

The industry operates under two primary business models: Integrated Device Manufacturers (IDMs), which manage all stages internally, and fabless companies, which focus on design and outsource manufacturing to foundries. This segmentation allows for specialization but also creates dependency on global supply networks. Semiconductor manufacturing is dominated by three types of chips: logic, memory, and analog. The sophistication of these chips is measured in nanometers, with the most advanced logic chips operating at 2–3 nm.

The global value added by semiconductor manufacturing was $445 billion in 2019 (see image below). Fabrication contributed the most (38.4%), followed by design (29.8%) and fab tooling (14.9%). As the industry grows, these proportions are expected to remain consistent, reflecting the critical roles of design and fabrication in the semiconductor supply chain.

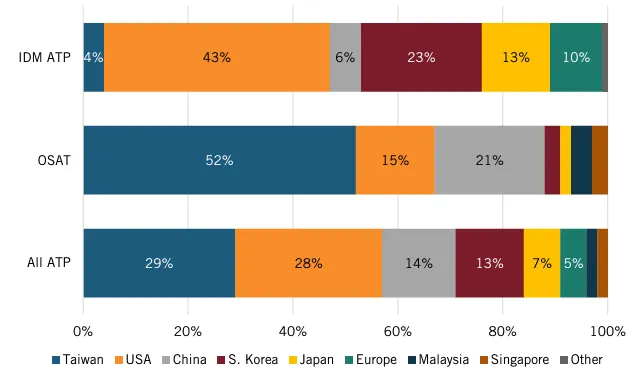

India’s Growing Role in Semiconductor ATP Market

The ATP market refers to the Assembly, Testing, and Packaging segment of the semiconductor industry. While there is significant activity for firms in the United States and Taiwan, the actual ATP activities are highly concentrated in Asia, particularly in China and Taiwan, which account for 75% of the total global ATP market combined.

Given its recent successes in attracting investment from companies like Micron, India is well-positioned to expand its role in the ATP segment. The proximity to the broader electronics manufacturing ecosystem , cost competitiveness, and supportive government policies can further boost India’s position in this market.

As evidenced by other countries' experiences, India could replicate the strategy of entering the semiconductor market through ATP and gradually moving up the value chain to fabrication and advanced semiconductor manufacturing. Micron's investment and subsequent interest from other players highlight the growing confidence in India's semiconductor ambitions.

Government Initiatives and Incentives for the Semiconductor Industry

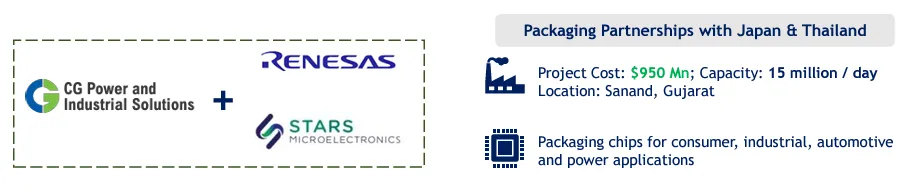

In recent years, the Government of India has launched the India Semiconductor Mission (ISM), committing approximately USD 10 billion to boost domestic semiconductor manufacturing. The incentives under this program include a 50% subsidy on semiconductor projects such as foundries, ATMP (Assembly, Testing, Marking, and Packaging) units, and display fabs, with additional state-level incentives contributing another 20-25% . So far, India has attracted INR 1.5 trillion in semiconductor investments from major companies such as Micron, Tata Electronics, CG Power, and Kaynes Technology.

To further boost local manufacturing, the Production-Linked Incentive (PLI) Scheme offers 4-6% incentives on incremental sales of domestically manufactured products, helping companies scale their operations.

The Indian government’s “Chips to Startup” (C2S) program, in collaboration with companies like Synopsys, aims to create a skilled workforce by partnering with over 400 universities.

In addition to manufacturing, India is focusing on skilling its workforce, with plans to train 85,000 professionals in semiconductor design, fabrication, and packaging. India already contributes 20% of the global semiconductor design talent, and this initiative will further strengthen the country’s capabilities.

The government is also promoting collaborations with countries like the US and Japan to secure critical raw materials and technology partnerships, ensuring India’s semiconductor industry is globally competitive and self-reliant.

Developing a Domestic Ecosystem for Semiconductor Manufacturing

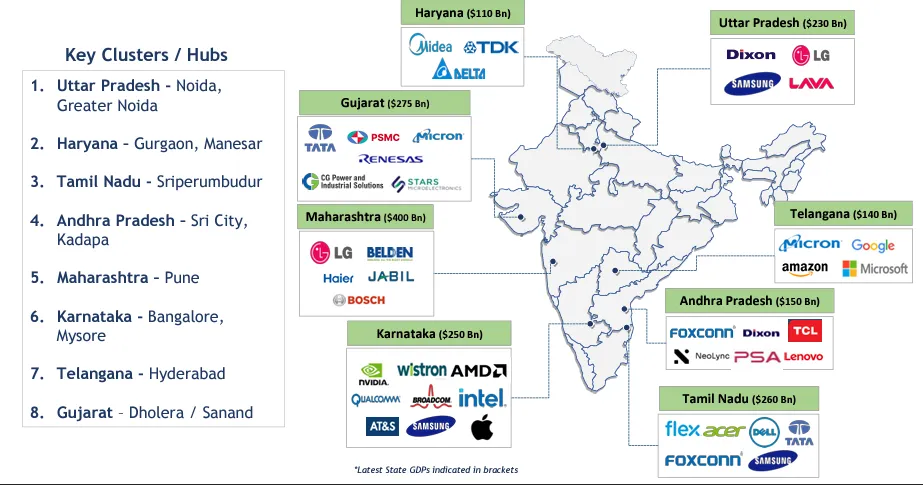

While multinational corporations dominate India’s semiconductor design landscape, the domestic ecosystem is slowly maturing. As of early 2023, India had about 21 start-ups in semiconductor design and manufacturing, with projections to reach 50 by year-end. Mindgrove Technologies, a Chennai-based start-up, is noteworthy for developing systems-on-a-chip (SoC) for connected devices. It aims to fill a market gap by offering chips that balance cost, power optimization, and performance—targeting applications such as smart meters and automotive devices. There are significant clusters for electronics manufacturing in India (see image below), where semiconductor clusters are also starting to form.

Other notable domestic players include Saankhya Labs and Signalchip. Saankhya Labs, established in 2006, was India’s first fabless semiconductor solutions company and is known for developing software-defined radios for applications like 5G and rural broadband. Signalchip focuses on high-speed wireless communication chips, aiming to support the country’s growing 4G and 5G infrastructure needs.

Key Investments and Collaborations

While India has traditionally been strong in integrated circuit (IC) design, the country is now focused on building a full-scale semiconductor manufacturing ecosystem. Initiatives like the upcoming OSAT facility by Kaynes Technology, which will package 6 million chips per day, reflect the country’s readiness to transition from design to manufacturing. Key players like Tata Electronics and Micron are setting up advanced semiconductor manufacturing facilities in India.

Lam Research, a global semiconductor equipment manufacturer, has committed to training up to 60,000 Indian engineers through its Semiverse Solutions platform, as well as investing $25 million in a new lab in Karnataka.

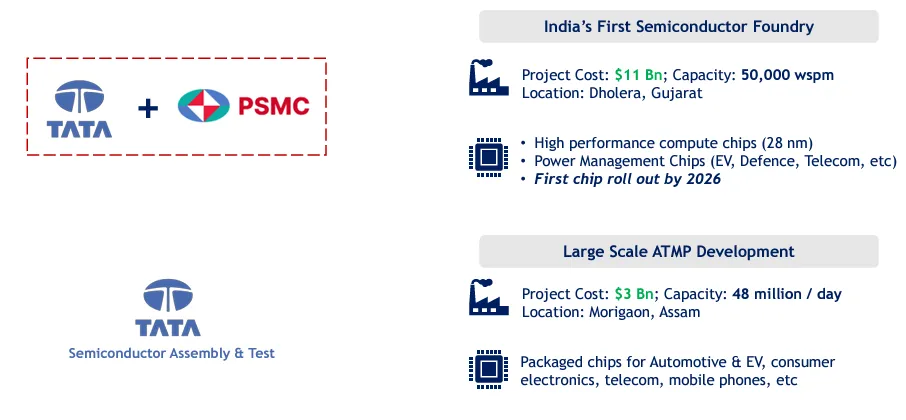

Tata’s foundry in Dholera, Gujarat, in collaboration with Taiwan’s PSMC, will manufacture 28nm chips.

Applied Materials, another leading toolmaker, has announced a $400 million investment over four years to establish a new engineering center in India. This center will support over $2 billion of planned investments and create over 500 new jobs, underscoring India’s growing importance as a hub for semiconductor manufacturing equipment design.

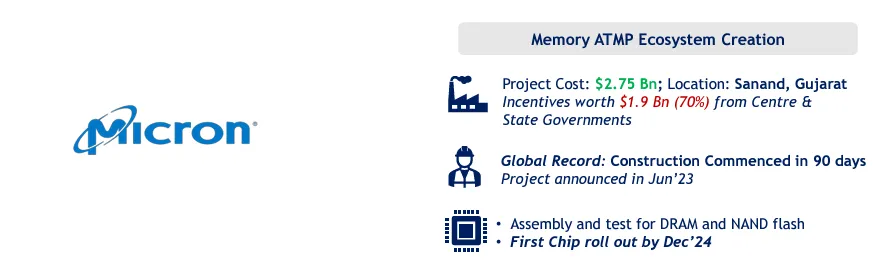

Micron’s ATMP facility in Gujarat will focus on assembling and testing DRAM and NAND flash modules, crucial for global semiconductor supply chains.

MD is also investing $400 million to set up a new design center for R&D and engineering in Karnataka, reinforcing India’s growing role in the global semiconductor ecosystem.

Additionally, there are upcoming projects from companies like CG Power, Kaynes, and Adani.

Semiconductor Partnership & Collaboration Between US & India

Funding and Infrastructure: The U.S. CHIPS and Science Act’s $500 million ITSI Fund could be used to establish partnerships with Indian and Quad-nation stakeholders, including setting up joint prototyping testbeds and R&D centers focused on chip design, foundry interests, and embedded systems.

Manufacturing and Centers of Excellence: Establishing up to 25 Electronic Manufacturing Centers in India as domain-specific Centers of Excellence with minimal funding could significantly boost the manufacturing ecosystem.

Workforce Development: India can play a crucial role in supplying skilled talent. Collaborative efforts in workforce education and training are needed, particularly to address the shortage of qualified faculty for semiconductor-related courses.

Partnerships in Education and R&D: A recent MOU between India’s Semiconductor Mission and Purdue University aims to develop advanced academic programs in semiconductor fields for Indian students.

Research Cooperation: A May 2023 agreement between the U.S. National Science Foundation and India’s Department of Science and Technology (DST) enables joint research proposals with a single review process.

Critical Minerals Supply Chain: India’s recent inclusion in the Minerals Security Partnership offers a strategic opportunity to collaborate on securing critical mineral supplies essential for semiconductor production.

Key Semiconductor Players and Indian Stocks to Watch

The semiconductor value chain is complex, encompassing multiple stages from design and fabrication to assembly, testing, and packaging. India, with its ambitious semiconductor strategy, is positioning itself across several segments of this value chain.

Let’s break down the key components and highlight Indian stocks involved in this ecosystem.

1. Semiconductor Foundries

Foundries are the backbone of semiconductor manufacturing. They fabricate chips based on designs provided by semiconductor companies.

Tata Electronics is leading the charge in India, with a foundry being set up in Dholera, Gujarat. The company has partnered with Taiwan’s PSMC to manufacture 28nm chips. This is a significant move for India’s entry into chip manufacturing.

Stock to watch: Tata Group companies, like Tata Elxsi (NSE: TATAELXSI), might benefit indirectly due to its involvement in design and tech.

2. OSAT (Outsourced Semiconductor Assembly and Test)

OSAT companies play a critical role by assembling and packaging chips for semiconductor manufacturers.

Kaynes Technology (NSE: KAYNES) is building an OSAT facility in Telangana with an initial capacity of 6 million chips per day. This facility will generate revenue from both legacy and advanced packaging.

Micron Technology is another key player establishing an ATMP facility in Gujarat. While Micron itself is not listed on Indian exchanges, this venture can impact suppliers and partners in India.

3. ESDM (Electronics System Design and Manufacturing)

India’s strength in the semiconductor value chain lies in its vast talent pool for design. Electronic Design Automation (EDA) tools and intellectual property (IP) play a major role in this phase.

Tata Elxsi (NSE: TATAELXSI) and Sasken Technologies (NSE: SASKEN) are two Indian companies offering EDA services and contributing to the semiconductor design process.

4. Compound & Discrete Semiconductor Manufacturing

This involves the production of specific semiconductors, such as SiC (Silicon Carbide) chips, which are essential for industries like automotive and energy.

RIR Power Electronics is setting up India’s first SiC power semiconductor plant in Odisha. Although not publicly listed, this project is set to transform India’s role in specialized semiconductor manufacturing.

Stock to watch: CG Power (NSE: CGPOWER), due to its involvement in power solutions, is likely to benefit from these advancements.

5. Equipment and Materials Providers

Semiconductor manufacturing requires specialized equipment, wafers, gases, and chemicals.

While India lacks a major presence in wafer manufacturing, local companies such as Sterlite Technologies (NSE: STRTECH) are making strides in providing fiber optics and critical infrastructure for semiconductor plants.

Linde India (NSE: LINDEINDIA), a supplier of industrial gases, is another crucial player in supporting semiconductor production through the supply of gases like nitrogen, oxygen, and argon.

6. Assembly and Testing

After fabrication, chips need to undergo rigorous testing and packaging before they can be integrated into final products.

Tata Electronics is again a key player here, with its assembly and testing facility in Jagiroad, Assam. This facility will focus on key packaging technologies such as Wire Bond and Flip Chip.

Challenges in Semiconductor Manufacturing

Despite its strengths in design, India’s lack of semiconductor fabrication capabilities remains a significant barrier. Indian chip designers must send their designs abroad for prototype development and testing, leading to increased costs and longer development cycles. Additionally, there is a cultural gap in innovation, with Indian designers more accustomed to following specifications than initiating them.

VC investment is another challenge. Semiconductor start-ups require sustained funding, often with long lead times before returns materialize. In 2022, VC investment in India fell by 38% to $20.9 billion, significantly lower than China’s $69.5 billion. This funding shortfall poses a significant obstacle to scaling India’s semiconductor ambitions.

Emerging Opportunities in Compound Semiconductors

An area where India could gain a competitive edge is in compound semiconductors, such as silicon carbide and gallium nitride (GaN). These materials are well-suited for high-power and high-frequency applications, making them essential for emerging technologies in sustainability and electrification. The global market for GaN semiconductors, valued at $2.17 billion in 2022, is expected to grow at a 25.4% CAGR through 2030.

Agnit Technologies, an Indian start-up, is working on GaN semiconductors, particularly for 5G amplifiers. However, funding and infrastructure are significant hurdles. To compete in this high-growth sector, India will need to develop both the physical and financial infrastructure to support innovation and manufacturing.

Future of Semiconductors in India

India is at a pivotal juncture as multinational companies seek to diversify supply chains and bolster production resilience. The country presents a compelling case as an investment destination for high-tech industries, particularly in semiconductors. India is already a key player in global semiconductor value chains, with significant contributions in R&D and design. To fully capitalize on this opportunity, India must continue to strengthen its semiconductor engineering workforce and ensure a supportive policy and regulatory environment. Consistent and predictable policies are essential for attracting and sustaining investments in this sector.

Collaboration between India and the United States is crucial in advancing these goals. The U.S.-India Semiconductor Supply Chain and Innovation Partnership aims to deepen cooperation in areas such as developing microelectronics curricula, facilitating student exchanges, and advancing joint R&D projects. This partnership also focuses on improving business conditions and investment flows, with active industry involvement being key to its success.

India has a unique opportunity to enhance its role in the global semiconductor supply chain and contribute to overall supply chain resilience. Through strategic collaboration, both India and the U.S. can achieve significant benefits, advancing their shared objectives in the semiconductor industry.

Our Investment Philosophy

Learn how we choose the right asset mix for your risk profile across all market conditions.

Subscribe to our Newsletter

Get weekly market insights and facts right in your inbox