by Alina Khan

Published On Aug. 14, 2023

In the dynamic world of investments, where fortunes can sway from triumph to turbulence in a heartbeat, the mastery of understanding and navigating portfolio risk emerges as a beacon of paramount importance. It is important to define portfolio risk to understand the risk you are taking on by investing in the stock market.

Portfolio Risk is a term used to describe the potential for losses within an investment portfolio. It is the uncertainty related to the return on a portfolio, consisting of different assets, each having its own risk profile. The risk in a portfolio could stem from individual security risks and how they interact with each other. There are different types of portfolio risk and in most cases we can take specific steps to mitigate these away.

As an example, let’s consider 2 people who have their own investment strategies.

One embraces the allure of high returns through stocks alone, disregarding potential risks.

The other understands the risks of the stock market and recognizes the trade-off between returns and risks. This person decides to diversify into bonds. Bonds, while generally safer than stocks, still harbor their own risks.

When the stock market eventually crashes, both of these persons will face losses in their stock investments.

However, the latter person’s foresight shines as the bond investments act as a safety net, cushioning the blow.

This narrative underscores the wisdom of spreading investments across multiple assets to help reduce the portfolio risk. The 2nd person's adeptness in assessing portfolio risk emerges as the key to recuperating and mitigating losses effectively. Successful investing is an intricate blend of seizing opportunities and erecting shields against potential losses. In this article we define portfolio risk, types of portfolio risk, how to calculate portfolio risk, factors & strategies influencing portfolio risk and more.

Let's look at what is portfolio risk and define portfolio risk first. Portfolio risk encompasses the uncertainty and potential for financial loss that is intricately woven into the fabric of investment portfolios . The very essence of risk arises from the dynamic interplay of various factors—ranging from the natural volatility of financial markets to the unexpected twists of geopolitical events. At its core, portfolio risk signifies the likelihood that the actual returns of an investment may stray from its anticipated returns. Here's a closer look at the key elements to help us understand what is portfolio risk and define portfolio risk better:

The standard deviation and variance are statistical measures used to quantify the dispersion of returns around the mean. A higher standard deviation indicates higher volatility and, therefore, greater risk. In the context of a portfolio, these measures help assess the overall risk based on the variability of each asset's returns.

The correlation coefficient between the assets in a portfolio measures how the returns of different assets move in relation to each other. Covariance is used to determine the extent to which two assets' returns move together. By combining assets with low or negative correlations, investors can reduce the overall risk of the portfolio. Diversification leverages this concept to minimize unsystematic risk.

Beta measures the sensitivity of a portfolio's returns to market movements. A portfolio with a beta greater than 1 is expected to be more volatile than the market, while a beta less than 1 indicates less volatility. Beta helps investors understand the extent of market risk in their portfolio.

Value at Risk is a statistical technique used to estimate the maximum potential loss of a portfolio over a given time frame at a specified confidence level. VaR provides a quantifiable measure of risk, allowing investors to gauge the potential impact of extreme market movements.

These techniques involve simulating various market conditions and scenarios to assess the potential impact on the portfolio. Stress testing evaluates how extreme market events would affect the portfolio, while scenario analysis examines the impact of specific hypothetical situations.

Portfolio at Risk is a measure used to quantify the potential loss in value of an investment portfolio over a specified period due to adverse market movements. It helps investors understand the risk associated with their portfolio and make informed decisions to mitigate potential losses. Portfolio at Risk is typically expressed as a percentage of the total portfolio value and can vary based on the types of assets held and their respective volatilities. By evaluating Portfolio at Risk, investors can adjust their asset allocation to manage risk more effectively and ensure their portfolio aligns with their risk tolerance and investment goals.

Now that we defined portfolio risk, let's look at the different types of portfolio risk converge before we understand how to calculate portfolio risk:

Market Risk: Navigating the investment landscape, one encounters an array of risks, and towering above them is the formidable market risk, also dubbed as systematic risk. Aptly named, this risk stems from the market's inherent volatility, casting a shadow over portfolios. Within this realm of market risk, distinct manifestations take form: equity risk, interest rate risk, and currency risk. Market Risk, also known as systematic risk, is associated with the broader market's unpredictability. Three sub-categories define this risk:

Equity Risk: The risk stemming from fluctuations in stock market prices. It materializes as the unsettling prospect of losing capital in the wake of a stock market decline. Investments intertwined with the stock market ride the tide of its fluctuations, potentially leading to financial erosion.

Interest Rate Risk: The risk related to changes in interest rates, particularly relevant for debt investments. Debt investments are particularly susceptible, as alterations in interest rates can trigger losses or gains.

Currency Risk: This relates to the risk of loss due to variations in foreign exchange rates. A shifting exchange rate can diminish returns when converted back to the investor's currency.

Liquidity Risk: This risk arises when an investor is unable to sell an investment quickly without a substantial loss in value. Liquidity Risk can be detrimental in emergency situations where cash is needed promptly. Investments are held hostage by low market values.

Concentration Risk: Concentration Risk is the risk associated with investing heavily in a single asset type. The peril here lies in channeling all financial resources into a solitary asset category, like the stock market. Diversification across different asset classes can help in mitigating this risk and shows the importance of a well-balanced investment portfolio.

Credit Risk: In the context of bonds, credit risk is concerned with the financial stability of the bond issuer. It manifests when the issuer of bonds grapples with financial troubles, jeopardizing the return of investment. Caution is a virtue; checking credit ratings of bonds before investment can help in understanding this risk better.

Reinvestment Risk: When interest rates fall, the risk that an investor may not be able to reinvest and attain the same returns as previously is known as Reinvestment Risk. Imagine investing in bonds at an attractive rate, reaping substantial rewards. Yet, as interest rates descend, the capacity to reinvest at that initial alluring rate wanes, diminishing potential returns.

Horizon Risk: Unexpected events forcing the sale of investments at an unfavorable time constitute Horizon Risk. This could lead to losses if the market is down during the sale. Picture a decade-long commitment, unforeseen events can thrust the investor into a corner, compelling untimely asset liquidation despite a market downturn, resulting in untoward losses.

In the labyrinth of investment, understanding and navigating these nuanced risks is a testament to an investor's acumen. It underscores the criticality of crafting a diversified portfolio, keenly monitoring credit ratings, and comprehending the intricate dance of market forces. Each risk is a thread, woven into the grand tapestry of investment, demanding astute management to unravel its potential impact.

Portfolio risk calculation is a nuanced endeavor often accomplished through statistical tools, the most prominent of which is the standard deviation . This statistical measure gauges the dispersion of an investment's returns around its average, offering insights into its inherent volatility. In other words, it measures the variance of specific returns compared to the average of those returns. Beyond individual asset risk assessment, modern portfolio theory amalgamates these individual risks to comprehend their collective interplay. Let’s look how to calculate portfolio risk, first we start with portfolio return -

Return on a portfolio is calculated as a weighted average of the individual returns of the assets within it. The weights represent the proportion of the investment in each asset, and the sum of these weights must be equal to 1.

Example:

Investment in Asset 1: Rs. 60,000 with 20% returns (Weight: 60%)

Investment in Asset 2: Rs. 40,000 with 12% returns (Weight: 40%)

Let's calculate the portfolio returns using the weighted average formula:

RP = w1R1 + w2R2 = 0.60×20%+0.40×12%=16.8%

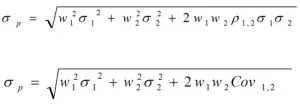

The risk of a portfolio isn't merely a weighted average of the risks (standard deviations) of individual assets. Instead, it also considers the correlation or covariance between the assets, reflecting how they move together.

The formula for portfolio risk involves calculating the standard deviation of the portfolio's returns, which considers the individual risks of the assets as well as their correlations. The general formula for portfolio risk (σp) for a two-asset portfolio is:

Example:

Standard Deviation of Asset 1: 10

Standard Deviation of Asset 2: 16

Correlation between the two assets: -1

The portfolio risk calculation is the portfolio's standard deviation:

σP = Sqrt(0.6^2*10^2 + 0.4^2*16^2 + 2*(-1)*0.6*0.4*10*16) = 0.4

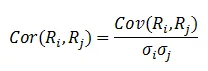

These measures are used to determine how two assets move in relation to each other. While correlation measures the strength and direction of the relationship, covariance quantifies it. They are related, and either can be used to calculate the standard deviation of the portfolio. It is calculated as follows -

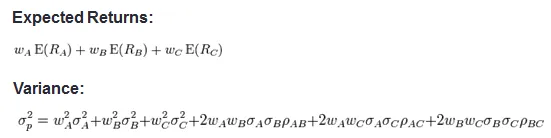

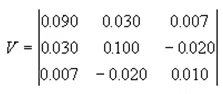

In our example, we simply had 2 assets. But as the constituents of the portfolio increase, as the number of assets increase - the complexity also increases and we consider the covariance between each pair of assets in a portfolio. A 3 asset portfolio risk calculationand return calculation is calculated as follows -

Using matrix multiplication we can simply the complexity that is involved with multiple assets in a portfolio. The variance covariance matrix is crucial here, with the variances of the assets as the diagonal elements and the covariances as the other elements.

For example, in Excel, the MMULT function can perform matrix multiplication, assisting in the calculation for portfolios with multiple assets. If we take the above example of a 3 asset portfolio with weights 30%, 30% & 40%, the covariance matrix is as follows -

And the variance of the portfolio is:

To learn more about portfolio risk and standard deviation, read our article on What is Standard Deviation and How Does it Help in Portfolio Management?

Portfolio risk is a multifaceted interplay of variables that warrants consideration:

Asset Allocation: The distribution of assets within a portfolio wields a significant influence over its exposure to risk.

Diversification: The strategy of spreading investments across diverse asset classes serves as a potent risk mitigation tool.

Economic Indicators: Market volatility is often mirrored by prevailing economic trends, underscoring the linkage between market stability and broader economic indicators.

Geopolitical Events: Global occurrences, from political shifts to geopolitical tensions, possess the potential to trigger market upheavals, impacting portfolio stability.

Portfolio risk management involves strategies to minimize the impact of various risks. Crafting strategies to attenuate risk of a portfolio is a dynamic process that demands a blend of insight and adaptability:

Diversification: The quintessential principle of spreading investments across different assets diminishes the impact of the downfall of any single asset.

Asset Allocation: Adapting the allocation of assets in response to risk appetite and evolving market conditions is a proactive measure to manage risk of a portfolio.

Utilization of Modern Portfolio Theory (MPT): MPT emphasizes a strategic mix of non-correlated assets to achieve a balance between risk and return

Risk-Adjusted Returns: Evaluating investments through the lens of risk-adjusted returns allows investors to assess the true potential of an investment while considering its inherent risk.

Hedging: Employing financial instruments like derivatives for hedging purposes can act as a protective shield against potential losses.

Inclusion of Liquid Assets: Adding liquid assets allows investors to access funds without having to sell volatile assets at a loss and reduce the risk of a portfolio.

Changes in an investor's financial goals and risk tolerance, along with fluctuations in market conditions make it imperative for us to conduct regular portfolio reviews and evaluation. Any necessary adjustments to the asset allocation mix, diversification strategies, and risk management can be executed in response to these assessment.

Asset allocation refers to the way an investor divides their total funds across different investment classes, such as equity and debt.

Example: An investor with a moderate risk tolerance may split their investment into 50% equity and 50% debt funds. Over time, changes in the NAV (Net Asset Value) of the funds may cause the allocation to shift, e.g., to 43% debt and 57% equity.

A regular review ensures that the asset allocation aligns with the investor's risk tolerance and financial objectives. If the equity component has increased disproportionately, the investor might be taking on more risk than they originally intended.

What should you do to maintain your asset allocation mix? Rebalancing the portfolio can restore the asset allocation mix to its optimal level, ensuring that it aligns with the investor's original profile.

Conduct a full portfolio review and analysis with Wright Research’s Portfolio Review Tool , for free.

Risk tolerance and life goals may evolve over time. While a younger investor might be willing to take more risks, this may change as they approach retirement or face new financial objectives.

Example: An initial 40:60 debt-equity mix may become 35:65 after 3 years. If the investor now wants to focus on retirement savings, they may wish to reallocate more funds to debt to earn steady returns.

Regular portfolio review offers an opportunity to assess whether the investments align with current and future goals, allowing for adjustments in line with new priorities or changes in risk appetite.

What should you do when your life goals and risk tolerance change? Reconstituting the portfolio to cater to new goals like retirement planning or updated risk tolerance levels ensures that the investment strategy remains relevant and effective.

Check your risk tolerance level and get a full risk assessment and analysis with Wright Research’s Risk Tool , for free.

Market conditions fluctuate, and periodic portfolio review can enable an investor to capitalize on these movements. They can reallocate funds to benefit from anticipated market trends.

Example: If the equity market is expected to perform well, an investor might increase their equity fund allocation. Conversely, if a bearish phase is anticipated, they might shift more into debt funds.

This proactive approach enables the investor to align their portfolio with market opportunities, potentially enhancing returns or protecting against downside risk.

What should you do to take advantage of market movements? By actively rebalancing in response to market predictions, the investor can maintain a portfolio that is responsive to the current investment environment.

Check our market dashboard to understand how the market is moving and to take advantage of market movements, explore Wright Research’s smallcases and mutual fund baskets .

In the intricate dance of investments, portfolio risk holds a central role, both as a challenge and an opportunity. Understanding its dimensions, the varied types that underlie it, and the factors that conspire to influence it, empowers investors to navigate the complex financial landscape with prudence.

Building a robust investment portfolio is not solely about capturing gains but also about fortifying against potential setbacks. By adhering to calculated strategies, consistently reassessing risk factors, and embracing the principle of diversification, investors pave the way for portfolios that stand resilient amidst the complexities of the market. These portfolios are poised to not only weather storms but to seize the opportunities that inevitably arise in the ever-shifting tides of the investment realm.

What is the significance of diversification in reducing portfolio risk?

Diversification spreads investments across various assets, reducing the impact of a single asset's poor performance on the entire portfolio, thus mitigating overall risk.

What is the relationship between risk and return in a portfolio?

Generally, higher potential returns are linked to higher risk in a portfolio. Investors aim to strike a balance between risk and potential reward based on their risk tolerance.

How can I assess the risk and return of my investment portfolio?

Evaluate historical performance, asset allocation, and volatility to assess both risk and return in an investment portfolio.

How do life events and changing financial goals impact portfolio risk?

Life events and evolving financial goals can alter risk tolerance, prompting adjustments to asset allocation and investment strategies.

What are risk-adjusted metrics, such as the Sharpe ratio and Sortino ratio, and how can they help me make better investment decisions?

Metrics like the Sharpe ratio and Sortino ratio measure risk-adjusted returns, factoring in the volatility of investments. They guide decisions by offering a more comprehensive view of performance.

How do Wright Research help investors in reducing portfolio risk?

Wright Research offers tailored investment strategies, diversified portfolios, and risk assessment tools. Their expertise guides investors in making informed decisions to mitigate portfolio risk.

Discover investment portfolios that are designed for maximum returns at low risk.

Learn how we choose the right asset mix for your risk profile across all market conditions.

Get weekly market insights and facts right in your inbox

Get full access by signing up to explore all our tools, portfolios & even start investing right after sign-up.

Oops your are not registered ! let's get started.

Please read these important guidelines

It depicts the actual and verifiable returns generated by the portfolios of SEBI registered entities. Live performance does not include any backtested data or claim and does not guarantee future returns

By proceeding, you understand that investments are subjected to market risks and agree that returns shown on the platform were not used as an advertisement or promotion to influence your investment decisions

Sign-Up Using

A 6 digit OTP has been sent to . Enter it below to proceed.

Enter OTP

Set up a strong password to secure your account.

Skip & use OTP to login to your account.

Your account is ready. Discover the future of investing.

Login to start investing on your perfect portfolio

A 6 digit OTP has been sent to . Enter it below to proceed.

Enter OTP

Login to start investing with your perfect portfolio

Forgot Password ?

A 6 digit OTP has been sent to . Enter it below to proceed.

Enter OTP

Set up a strong password to secure your account.

Your account is ready. Discover the future of investing.

By logging in, you agree to our Terms & Conditions

SEBI Registered Portfolio Manager: INP000007979 , SEBI Registered Investment Advisor: INA100015717

Tell us your investment preferences to find your recommended portfolios.

Choose one option

Choose multiple option

Choose one option

Choose one option

Choose multiple option

/100

Investor Profile Score

Congratulations ! 🎉 on completing your investment preferences.

We have handpicked some portfolios just for you on the basis of investor profile score.

View Recommended Portfolios