Momentum investing is a lesser known trading strategy that works to break out of the trend of making educated bets on a particular company in its infancy in the hopes that a longer term hold will bring positive results. Instead, momentum trading uses technical analysis to identify undervalued stocks that have potential to rise, holding them short term, and selling them off at their peak.

“Momentum investing is a system of buying stocks or other securities that have had high returns over the past three to twelve months, and selling those that have had poor returns over the same period.”

Although seemingly an intuitive trading strategy, the ‘momentum’ aspect comes into play here through following a predetermined algorithm and benchmarks for any particular stock created by the trader, and using these indicators to pick stocks to buy, and inform the price changes at which they should enter/exit. It is a strategy that operates on a shorter time scale, informed by many high level analyses (Moving Average Convergence Divergence (MACD), Relative Strength Index (RSI), Stochastic Oscillator, and more), to identify and invest in stocks that are currently in an upward trend, with the expectation that the trend will continue in the near term., and vice versa with stocks in a negative trend

Momentum investing is a trading strategy that is strictly technical, that has no care for a company's operational performance. There is an inherently psychological aspect to momentum investing, as analysts are trying, if possible, to understand and anticipate the behaviours of other players in the market. It is a unique strategy, one that is driven by the juxtaposition of human behaviour and rational decision making, as well as rigorous quantitative analysis.

There are four major psychology linked facets that are used to understand the human aspect of momentum investing:

Herding Behaviour

Confirmation Bias

Overconfidence

Efficient Market Hypothesis

Herding Behaviour refers to the tendency of investing following the popular decisions of the majority, or ‘following the crowd’. It is often the case that investors will purchase trending stocks, or ones that are seemingly verified amongst other investors in behaviour that is driven by the ‘fear of missing out’ - commonly known as ‘FOMO’. This behaviour is also exacerbated by the desire and pressure to follow social norms, and to fit in with peers who may also be talking positively about a stock.

Another psychological factor that contributes to momentum investing is confirmation bias, which refers to the tendency of investors to seek out information that confirms their beliefs and ignore information that contradicts them. If an investor has made, say, a risky choice of investment, but later comes across reams of information endorsing this stock, they are more likely to feel supported in their decision and bolstered to remain investing in the same way, until it becomes a stock they now believe in. Their bias has now therefore been confirmed, and they may continue to buy this stock, even if new evidence emerges to suggest it may not be a great buy. These steps of decision making that have moved away from the desired rational investing tactics can lead investors to overlook important information and make poor investment decisions.

Overconfidence refers to the situation that occurs when an investor has previously experienced success with a stock, and blindly assumes that these trends will continue in the future. These feelings of overconfidence may influence their investment decisions, and lead them into making a poor and risky choice. Again, this may be in light of clear evidence suggesting they should do otherwise.

Finally, the Efficient Market Hypothesis. The efficient market hypothesis is a theory that assets in a market are fairly priced as they have been valued with all the information that is available to an investor. Therefore in this situation, it is impossible for any one individual to make large and sustained profits or losses through techniques like ‘timing the market’ or using experts to select stocks, and without taking large risks, as economically, the investor is expected to behave rationally. Because of this, some argue that the very reason momentum investing works is that because the market has already priced in all available information, any stocks that are trending upward should be assumed to continue to do so, and therefore, buying these stocks is a rational strategy that takes advantage of market inefficiencies.

However, this very reasoning seems paradoxical - if the market is efficient, then how can there be inefficiencies? Any observed momentum should not provide an opportunity to achieve abnormal returns, as the prices already incorporate all known information. It is a fine point being made here; that momentum under the Efficient Market Hypothesis is seen as a wholly rational decision to make, but it becomes momentum as one is simultaneously taking advantage of any market frictions like transaction costs, or any human responses like biases or delayed reactions to information. These slow reaction, or correctional, times cause a more gradual drift towards the new price, creating a small window of time that momentum investors can then exploit. This is why momentum investing is largely a short term strategy, dependent on trends in the market.

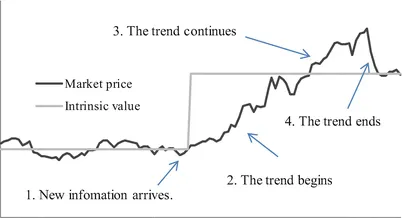

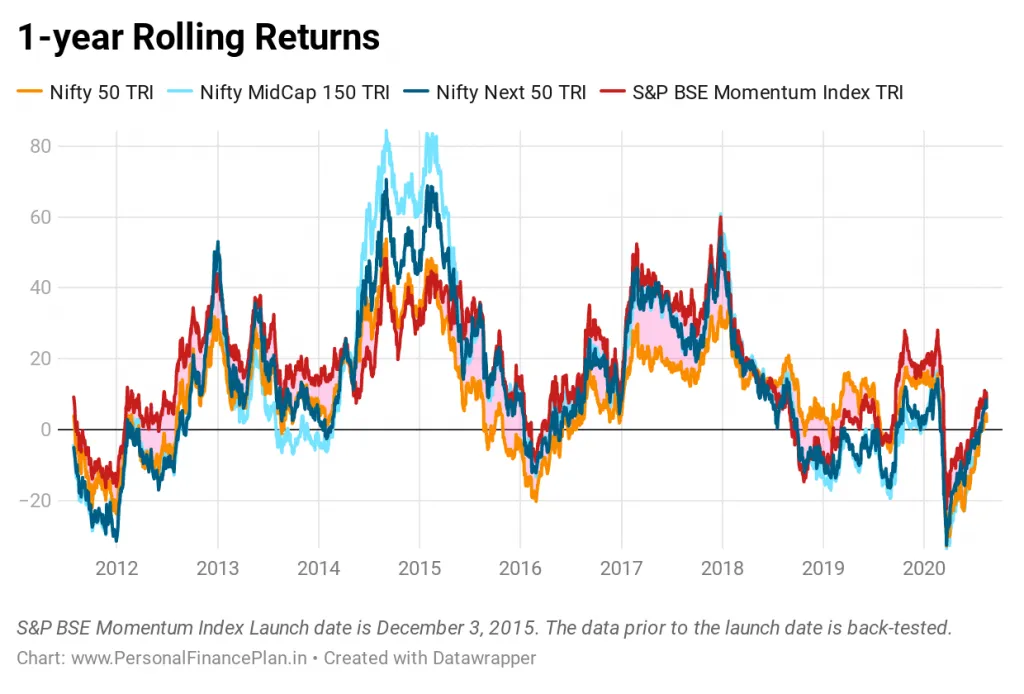

Figure 1

Academically, there has been much contention over the reason why the momentum anomaly exists, and continues to, despite individuals being cognisant of its existence, but much of the literature exploring this focuses on investors' behavioural traits, namely investor under-reaction or delayed over-reaction. Under-reaction happens when investors don't respond strongly enough to certain financial news. For instance, if a company reports strong quarterly earnings, the stock price may increase initially, but not as much as it should. Consequently, over the following weeks, the stock price may gradually rise as the market fully digests the information from the earnings report.

Momentum investing is effective because behavioural biases contribute to the persistence of price trends. Since investor behaviour is not always fully rational, these inefficiencies create opportunities for momentum strategies to generate returns by capitalising on trends driven by these market anomalies.

As evidenced, there are some limitations and peculiarities with trying to explain the phenomenon of momentum investing using the Efficient Market Hypothesis alone. This is where behavioural finance comes in, to offer compelling reasons as to why momentum works. In practice, the momentum effect is observed when stocks that have performed well (winners) continue to do so, while those that have performed poorly (losers) continue to underperform. This pattern contradicts the random walk theory, which suggests that past performance should have no bearing on future returns. However, numerous studies and empirical evidence suggest otherwise. Momentum strategy tends to work well across various market conditions and even when applied to smaller portfolios. The research also emphasises that the momentum effect is not just a statistical artefact but a real and exploitable market anomaly. Figure 1 illustrates how momentum portfolios consistently outperform the market index, providing visual evidence of the momentum effect's persistence.

Momentum has been extensively studied across different markets and time periods, consistently showing that stocks with strong past performance tend to continue performing well in the short to medium term. These studies provide robust evidence that momentum is not just a fleeting market anomaly but a persistent phenomenon across various asset classes and geographies. Research presented by Intalcon highlights that momentum portfolios consistently outperform market benchmarks across different economic cycles. This outperformance is attributed to the aforementioned behavioural biases, which lead to predictable patterns in asset prices. Momentum has been observed in global equity markets, commodities, currencies, and even bonds, suggesting that the underlying behavioural biases are universal.

Momentum is not confined to equities. Studies have shown that similar patterns exist in commodities, currencies, and other asset classes. For example, momentum in commodities often arises from supply and demand imbalances that take time to correct, while in currencies, it can result from central bank policies or macroeconomic trends that persist longer than anticipated.

Value and momentum returns tend to move together more strongly across different asset types compared to how passive investments in those asset types move. However, value and momentum tend to move in opposite directions, whether you look within the same asset type or across different asset types.

Momentum strategies are inherently risky, particularly because they rely on trends that can reverse suddenly. For instance, during market corrections or periods of high volatility, momentum stocks may suffer significant losses, as the market quickly shifts from risk-on to risk-off behavior. To mitigate these risks, investors often use a combination of momentum with other strategies, such as value investing, which tends to perform well when momentum falters.

Additionally, risk management techniques such as stop-loss orders, position sizing, and diversification are critical when implementing a momentum strategy. These tools help investors manage the downside risk while maintaining exposure to the upside potential that momentum strategies offer.

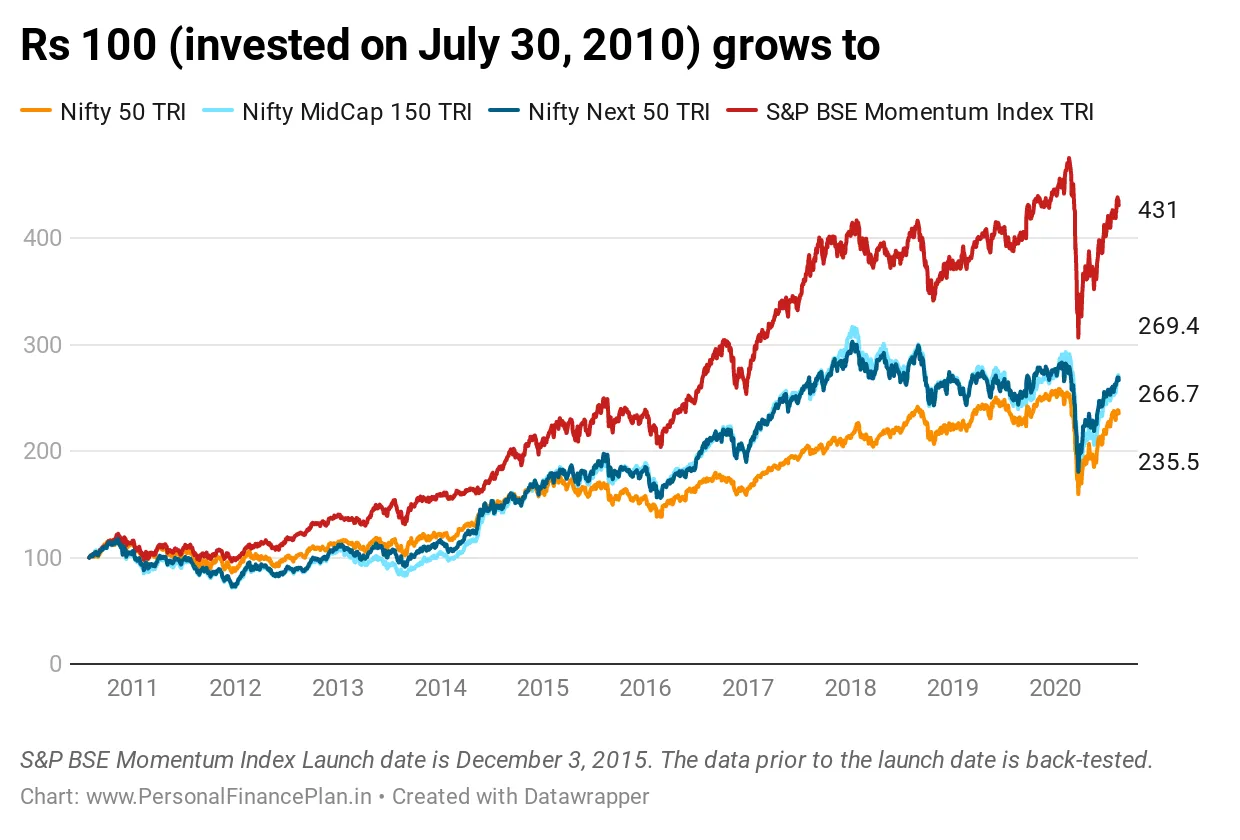

While momentum strategies yield attractive returns across asset classes, the associated risks also vary, as illustrated by Figure 2.

Figure 2

A study by Weimin Lui, Norman Strong, Xinzhong Xu, ‘The Profitability of Momentum Investing’, investigates the existence of momentum profits in the UK stock market from 1977 to 1998. Their research not only confirms the presence of significant momentum profits but also challenges the efficient market hypothesis, particularly its weak-form efficiency, by demonstrating that past returns can indeed predict future returns.

The authors utilise methodologies based on Lehmann (1990) and Jegadeesh and Titman (1993) to construct momentum portfolios. They rank stocks according to their past performance over specific periods—typically 3, 6, or 12 months—and then track the returns of the top-performing ("winner") and bottom-performing ("loser") portfolios over subsequent periods of similar length. The momentum profit, which is the return generated by the momentum strategy, is derived by calculating the difference between the returns of these winner and loser portfolios.

Mathematically, the return from the momentum strategy is expressed as:

Where:

W and L represent the sets of winner and loser stocks, respectively.

Rit is the return of stock i at time t.

Nw and Nl are the numbers of stocks in the winner and loser portfolios.

Their analysis, covering both a comprehensive sample of UK stocks and a sub-sample with detailed accounting data, confirms the robustness of momentum profits across different periods and conditions. To further explore the nature of these profits, the study controls for known risk factors using the Fama-French three-factor model, which accounts for market, size, and value factors:

Where:

Rit is the return of stock i.

Rmt is the return on the market portfolio.

Rft is the risk free rate.

SMBt (Small Minus Big) adjusts for the size effect.

HMLt (High Minus Low) captures the value effect associated with the book-to-market ratio.

Despite controlling for these variables, the study finds that momentum profits remain significant and cannot be fully explained by cross-sectional differences in average returns. This indicates that these profits are not merely a byproduct of known risk factors but rather represent a distinct phenomenon.

Further analysis examines whether serial correlation in common factors or delayed price reactions to these factors could explain the momentum profits. By evaluating the autocorrelation of returns and common factors such as market returns, the study determines that these factors do not account for the observed momentum profits. Consequently, the authors conclude that the momentum effect likely arises from the market’s underreaction to firm-specific or industry-specific information, which results in a gradual price adjustment that momentum strategies can exploit.

Liu, Strong, and Xu’s study highlights the presence of significant momentum profits in the UK market, driven by specific inefficiencies rather than broad market trends. Their findings suggest that investors can benefit from strategies that capitalise on the market’s slow reaction to new information, challenging the traditional views of market efficiency and providing a deeper understanding of the forces that drive stock prices.

India’s stock market is characterised by a diverse composition of large-cap, mid-cap, and small-cap stocks, with a substantial presence of retail investors. Unlike more developed markets, where institutional investors dominate and market efficiency is relatively high, the Indian market's structure allows for certain inefficiencies that can be exploited by momentum strategies. One key factor is the relatively delayed reaction to news and earnings reports among retail investors, which creates opportunities for momentum traders to profit from these lagging responses.

Additionally, the Indian market exhibits varying levels of liquidity and information asymmetry. While large-cap stocks generally enjoy higher liquidity and more efficient information dissemination, mid-cap and small-cap stocks are often subject to liquidity constraints and less transparent information flows. Even within the large-cap segment, the Indian market does not match the efficiency seen in developed markets, allowing momentum effects to persist as prices adjust more slowly to new information. These structural inefficiencies create a fertile environment for momentum investors, who can take advantage of the slower price adjustments to generate returns.

Empirical evidence strongly supports the viability of momentum investing in the Indian market. A study found that a momentum portfolio of Indian large-cap stocks consistently outperformed the broader market index over a 10+ year period, with annualised returns significantly higher than those of a passive index-tracking strategy.

This outperformance was especially pronounced in certain sectors, such as information technology and consumer goods, where the momentum effect appeared to be more robust. The study's findings suggest that momentum investing can be a powerful tool for generating alpha in the Indian market, particularly during bull markets where positive investor sentiment further amplifies the continuation of trends. "Alpha" refers to the additional return that an investment strategy, such as momentum investing, generates over and above the expected return based on the level of risk involved - it serves as an indicator of how much a strategy outperforms the broader market or a relevant benchmark.

In the context of this study, with the suggestion that momentum investing can be a powerful tool for generating alpha in the Indian market, particularly during bull markets, it means that this strategy has the potential to achieve returns greater than those typically expected from general market movements, especially when positive investor sentiment reinforces ongoing trends.

Momentum investing has seen a notable rise in India, fueled by the active participation of both institutional and retail investors. Leading the charge are institutional investors, such as quantitative funds and hedge funds, who have embraced momentum strategies with increasing enthusiasm. These sophisticated investors utilise advanced algorithms capable of identifying and exploiting trends across various market segments. By integrating machine learning and artificial intelligence into their trading models, they have significantly enhanced the precision and effectiveness of their momentum strategies, allowing them to capitalise on market trends with remarkable accuracy.

Alongside institutional players, retail investors are also becoming more involved in momentum investing, particularly through momentum-based exchange-traded funds (ETFs) and mutual funds. The Indian market has witnessed the launch of several momentum ETFs, providing retail investors with a convenient and straightforward entry point into this strategy. Typically, these funds track indices that are specifically designed based on momentum criteria, such as the Nifty 200 Momentum 30 Index. The combination of rising financial literacy and the proliferation of online trading platforms has further democratised access to momentum strategies, making them increasingly popular among a broader spectrum of investors.

The supportive regulatory environment in India, overseen by the Securities and Exchange Board of India (SEBI), has also been instrumental in the growth of momentum investing. SEBI’s initiatives to enhance market transparency, improve liquidity, and develop a robust financial ecosystem have created a favourable backdrop for the adoption of advanced investment strategies like momentum. As India’s financial markets continue to evolve and become more integrated with global systems, the use of momentum investing is likely to expand even further, driven by the ongoing maturation of the market and the increasing sophistication of investors.

The future of momentum investing in India looks promising, with several factors poised to drive its continued growth. As data availability improves and analytics technology advances, investors will have the tools to refine their momentum strategies further. The incorporation of machine learning and big data analytics is expected to yield more accurate models, allowing investors to better predict and take advantage of momentum effects, ultimately enhancing the effectiveness of these strategies.

Moreover, institutional interest in momentum investing is anticipated to grow, leading to the development of more sophisticated product offerings. These may include structured products that blend momentum with other investment themes, specifically tailored to the nuances of the Indian market. As institutional investors increasingly recognize the potential of momentum strategies within India, their participation is likely to expand, fostering further innovation and advancement in this field.

Additionally, the growing integration of Indian markets with global financial systems will inevitably impact the dynamics of momentum investing. With global trends and capital flows playing a more significant role in the Indian market, momentum strategies may need to evolve to account for these external influences, presenting both new opportunities and challenges for investors, who navigate an increasingly interconnected financial landscape.

Written by Sarah Essessien

Discover investment portfolios that are designed for maximum returns at low risk.

Learn how we choose the right asset mix for your risk profile across all market conditions.

Get weekly market insights and facts right in your inbox

It depicts the actual and verifiable returns generated by the portfolios of SEBI registered entities. Live performance does not include any backtested data or claim and does not guarantee future returns.

By proceeding, you understand that investments are subjected to market risks and agree that returns shown on the platform were not used as an advertisement or promotion to influence your investment decisions.

"I was drawn to Wright Research due to its multi-factor approach. Their Balanced MFT is an excellent product."

By Prashant Sharma

CTO, Zydus

By signing up, you agree to our Terms and Privacy Policy

"I was drawn to Wright Research due to its multi-factor approach. Their Balanced MFT is an excellent product."

By Prashant Sharma

CTO, Zydus

Skip Password

By signing up, you agree to our Terms and Privacy Policy

"I was drawn to Wright Research due to its multi-factor approach. Their Balanced MFT is an excellent product."

By Prashant Sharma

CTO, Zydus

"I was drawn to Wright Research due to its multi-factor approach. Their Balanced MFT is an excellent product."

By Prashant Sharma

CTO, Zydus

Log in with Password →

By logging in, you agree to our Terms and Privacy Policy

"I was drawn to Wright Research due to its multi-factor approach. Their Balanced MFT is an excellent product."

By Prashant Sharma

CTO, Zydus

Log in with OTP →

By logging in, you agree to our Terms and Privacy Policy

"I was drawn to Wright Research due to its multi-factor approach. Their Balanced MFT is an excellent product."

By Prashant Sharma

CTO, Zydus

Answer these questions to get a personalized portfolio or skip to see trending portfolios.

Answer these questions to get a personalized portfolio or skip to see trending portfolios.

(You can choose multiple options)

Answer these questions to get a personalized portfolio or skip to see trending portfolios.

Answer these questions to get a personalized portfolio or skip to see trending portfolios.

Answer these questions to get a personalized portfolio or skip to see trending portfolios.

(You can choose multiple options)

Investor Profile Score

We've tailored Portfolio Management services for your profile.

View Recommended Portfolios Restart